The US healthcare services industry is at a tipping point, but who—or what—is driving the undercurrents of change?

Over the past five years, institutional investors have been quietly shaping parts of the healthcare industry. Private equity (PE) investors, for example, have begun to consolidate several markets, including ambulatory surgery, hospitalist staffing, and home health, undertaking more than $50 billion in total transactions.

Institutional investors’ focus on healthcare services—healthcare delivery and its enablers—is likely to continue, given industry trends. Ongoing growth in health expenditures, the degree of medical waste, and industry fragmentation signal high upside potential. Furthermore, the impact on the industry could be even greater in coming years. Institutional investors have been learning from their experience and will likely be using those lessons as they inject hundreds of billions in capital into healthcare in the next five years. These new investments have the potential to drive structural shifts in ways that are more direct and proactive than have been used before.

Health systems must decide how they want to respond—inaction is no longer an option. As they consider their responses, the systems need to answer two questions: Do they want to shape the industry on their own or alongside the institutional investors? And, how can they transform their business models to be sustainable as the industry evolves?

How active have investors been, and will it continue?

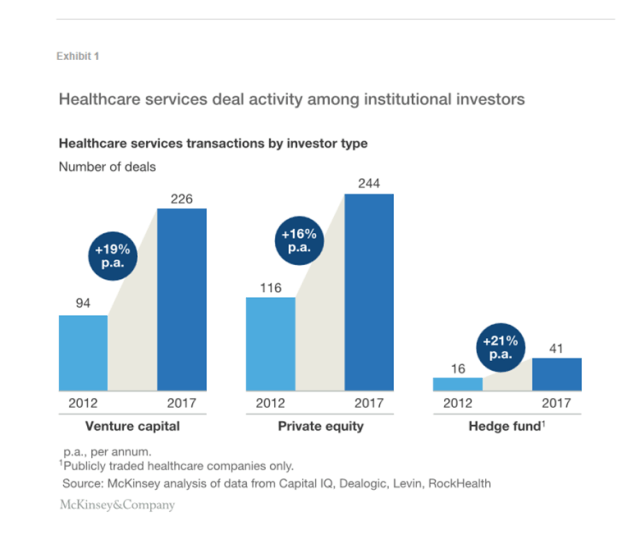

The degree of institutional investing in healthcare has accelerated. The number of deals has grown at a compound annual growth rate of 18% since 2012—PE, venture capital (VC), and hedge fund investors announced about 225 deals in 2012 but more than 510 in 2017.1 Each of these investor types has increased both its number of deals and share of overall healthcare investments. The capital inflow has been accompanied by high expectations for the return on invested capital (ROIC) and time frame within which returns would be achieved. These expectations have created tension with healthcare service providers and have shifted the providers’ expectations about how to deliver services and optimize operations to remain competitive, resulting in higher performance levels.

Because of the sums involved, institutional investors are now proactively shaping business models and submarkets within healthcare services. Exhibit 1 illustrates the magnitude of the fund flows.

Over the past five years, annual returns on investments in healthcare services have averaged about 10%,2 but some investments have paid off better than others. Multiple investors had predicted increased demand for healthcare services and changes in market dynamics following passage of the Affordable Care Act (ACA). Those who have kept their money focused primarily on those themes have not fared as well as those who refined their view and shifted their investments in response to changes in the industry. Nevertheless, institutional investors have been able to raise additional funds. Several factors suggest the capital inflow from institutional investors will continue.

Demand dynamics remain favorable.

Between 2012 and 2016, total overall healthcare EBITDA grew faster than did the combined EBITDA of the top 1,000 US companies.3 Growth in both the senior population and number of patients with chronic disease is likely to create a sustained increase in service demand. Healthcare spending in the United States is projected to rise by about 6% per annum through 2025 (assuming current care delivery trends continue).4

Economies-of-scale opportunity is clear.

Most healthcare service providers remain subscale and fragmented. The top five health systems together account for only about 13% of annual hospital admissions.5 Unsustainable cost pressures within the healthcare industry are leading to structural shifts, accelerating consolidation, a trend that lends well to investors’ efforts to create and leverage scale to unlock value-creation opportunities (e.g., centralization of back-office resources, improved supplier negotiations, increased patient volumes, and risk-based arrangements with managed care payers).

Conditions favor new business models.

Changing consumer preferences and pressures to reduce the total cost of care have led to service delivery innovations. One of the factors that has helped prompt these changes is regulatory: between 2013 and 2017, the Centers for Medicare and Medicaid Services increased reimbursement by 1% to 2% per annum for hospital-based surgical care but by 4% to 5% annually for similar procedures performed in ambulatory surgery centers.6 7 Additionally, technological advancements have made services and technology companies the fastest-growing profit pool in the healthcare industry.8

Access to investable platforms remains.

Fragmentation has also created investment opportunities. For example, ambulatory networks with less than 10 sites have EBITDA multiples in the low single digits, while some networks with more than 50 sites (e.g., a few large, metropolitan urgent care networks) have multiples in the low- to mid-teens. (Such large networks are still relatively rare in the healthcare services industry, however.) Furthermore, there has been a steady supply of new assets every year. VC firms have developed a significant pipeline, investing at least $20 billion in nearly 1,000 companies over the past five years.

Where has the activity been and where might it go?

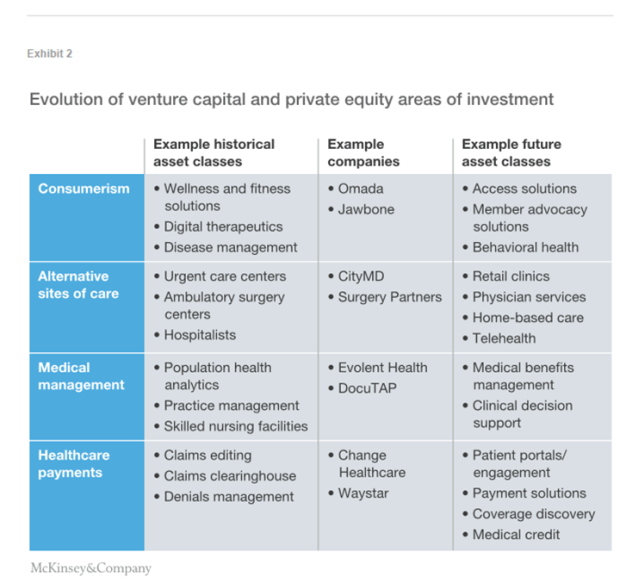

The question is not if institutional investments will continue, but rather where the money will be invested and what it will influence. We believe that the overarching focus in the next few years is likely to be on lowering the cost of care and reducing leakage in providers’ revenues. Healthcare services areas of interest are likely to be consumerism, alternative sites of care, medical management, and healthcare payments (Exhibit 2). However, the types of investment made within these areas will probably shift as industry dynamics continue to change, investors’ savvy in predicting service uptake increases, and investors become better advisors to the operators of the companies they invest in.

Consumerism

The profile of healthcare consumers has evolved in recent years—they are now more price sensitive and tech savvy, and put greater emphasis on convenience. In our 2017 Consumer Health Insights Survey, for example, 65% of commercial insurance respondents selected cost as a top area to better understand when choosing where to get healthcare, and 71% said they would use video or online doctor visits if such tools were offered by their primary care physician.9 We believe this evolution will continue.

Many investor bets on consumer-centric healthcare were initially placed on wellness and disease management solutions given to consumers via their healthcare provider or employer. However, these approaches failed to gain significant traction, given the fragmented care environment and their inability to demonstrate outcome improvements sufficient to justify their cost. In the future, we believe investments in consumerism will focus more on solutions that address under-served types of care or enable a more seamless patient experience. Most of these solutions will be geared to payers, providers, or employers—not patients—as buyers; more time is likely to be needed to document the improvements necessary to convince consumers to purchase the solutions.

Outpatient behavioral health is an example of a consumer-driven, unmet need. Future investments in behavioral health could focus on outpatient offerings (e.g., addiction clinics) or innovative solutions that integrate similar offerings with technology-enabled delivery to provide services to high-cost and/or high-risk populations. Quartet, for example, has begun to partner with health systems and payers alike to address high-need patients.

Alternatives in the provision of care

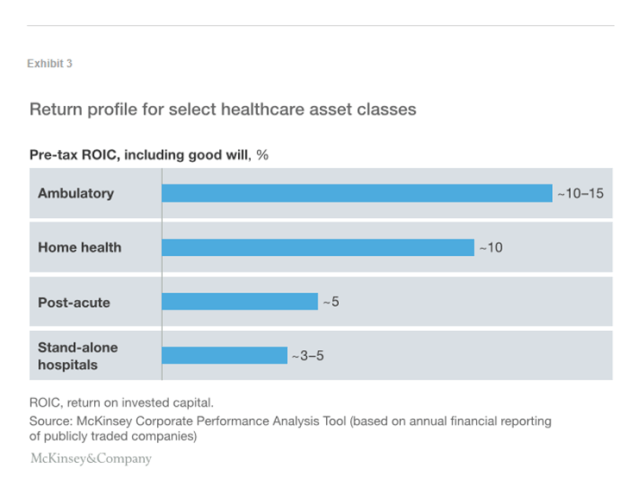

Increasingly, substitution is occurring in the provision of care—who provides it and where it is delivered. Shifts across asset classes have been driven by several forces: changes in reimbursement that favor lower-cost sites, health plan redesign to incentivize consumers to utilize lower-cost care settings (e.g., urgent care in ambulatory settings rather than hospitals; post-acute home health rather than facility-based care). Substitution within an asset class has largely focused on hospitals—cost and quality pressures have resulted in changes to the traditional business model. Many facilities, for example, have moved to outsourced hospital-based physicians (e.g., anesthesiologists and emergency physicians). The substitution effect, coupled with the newer asset classes’ better return on capital (Exhibit 3), has increased investors’ interest in two areas in particular:

Low-cost providers in need of capital to scale. Since 2012, PE investments in this area have increased by about 16% per annum. Examples include Warburg Pincus’s investment in CityMD; TPG’s in GoHealth; and Welsh, Carson, Anderson & Stowe’s in InnovAge. In these cases, the assets required capital to further scale locally or nationally. The continued emphasis on shifting to lower-cost providers will create ongoing opportunities for investment in retail-type care provision models (e.g., on-site employer clinics), home-based care (e.g., home health, personal care assistance), and remote health (e.g., e-visits, telehealth).

Physician groups that can provide care within alternate settings. Historically, investors have focused on hospital-based specialties that can be outsourced as a low-cost alternative to hospitals or specialties with higher exposure to private pay (e.g., dermatology). Looking forward, an increasing volume of investments will likely be made in areas that can deliver more convenient, lower-cost services for an aging population (e.g., orthopedics, gastroenterology, cardiovascular, oncology), especially given current dynamics within physician services. (The United States is projected to have a physician deficit of up to 88,000 providers by 2025.10 ) While these specialties have greater exposure to Medicare reimbursement, they also enable investors to access non-traditional value-creation levers. These levers include expanding ancillary offerings to shift day surgeries, imaging, and lab services from hospital-outpatient to free-standing settings; adopting risk-based arrangements to capture upside from managing the total cost of care; and investing in technology solutions to increase physician productivity and lower administrative burdens.

Medical management

Medical management

Historically, investments in medical management focused on population health analytics and direct ownership of the parts of the care continuum that were driving variation in costs. However, success has been difficult to achieve in these areas—population health analytics predicated on risk-based arrangements with downside risk (to align incentives) and payer-provider data integration are still in nascent stages of development. Achieving success in direct ownership of skilled nursing facilities, for example, requires business model transformation to unlock value, given reimbursement headwinds. To date, most investors have not had sufficient operational savvy to accomplish that.

In the future, reducing medical “waste” is likely to remain a priority. Many investments may therefore focus on data-driven services that might decrease utilization and improve unit-cost management. For example, investors will continue to help expand the historical success pharmacy benefits management achieved into other categories of benefits (e.g., medical oncology, post-acute care) and to specific types of patients (e.g., high-risk, behavioral). Nearly $1 billion in VC funding has already been invested in medical benefits management, which has created a pipeline of assets for PE firms.

As value-based care models continue to be implemented across the country, the need for clinical decision-support tools designed to reduce the cost of care and outcomes variability will grow. Although PE groups have yet to invest seriously in this area, decision-support companies have received more than $2 billion in VC funding since 2011—so uptake may be expected.

Optimizing healthcare payments

Each year, more than $3.5 trillion flows through the US healthcare system to providers. Employers and government are responsible for over 85% of these funds via payments to health insurers or directly to providers, but more than $200 billion is sent directly from consumers to providers.11 Given these sums, many investments have focused on the digitization and standardization of both payers’ payment integrity and providers’ revenue cycle management. However, the complexity of healthcare payments is increasing. As consumers take on a greater share of healthcare payments, it is becoming increasingly important that they be given an accurate estimate of the costs that will be billed to them before an encounter with a provider. Furthermore, “smarter” methods to predict and adjudicate payments are needed to account for risk- and quality-adjustment factors.12

Better approaches to payment are required if patients are to proactively manage out-of-pocket expenses, providers are to reduce consumer bad debt, and payers are to accurately anticipate medical expenses. For example, an integrated solution could give patients financial planning tools and an accurate idea of what their out-of-pocket costs are likely to be (based on their coverage), while also giving providers a way to estimate patients’ payments. If then combined with an online payment portal, the solution could reduce the complexity patients’ face with managing healthcare payments. New approaches might also include technology-enabled solutions that address pain points healthcare providers have in revenue cycle management, such as coverage discovery and point-of-service payment collections.

Investors are therefore likely to continue seeking new payment solutions, with a heightened focus on those that could fundamentally change how patients, providers, and payers understand and manage payments before an encounter. Investments will probably also accelerate for technology-based solutions that enable automated eligibility checks, cost and propensity-to-pay estimation, and point-of-service payment. More than $5 million in VC funding has already supported development of several patient payment companies.

How could these trends reshape the industry?

Deal activity is likely to accelerate, given average annual returns above 10% in healthcare services.13 The inflow of capital from institutional investors will make possible the development of new business models. This inflow, in combination with greater maturity in analytics and digital capabilities, wider implementation of risk-based reimbursement arrangements, and greater pressure from payers and consumers, could accelerate the pace of change in healthcare services. Areas of the value chain that could be disrupted include both the non-acute and post-acute care continuums, services analytics platforms, and care delivery operating models. The disruption could play out in at least six ways:

Healthcare as a service industry. Increased access to lower-cost settings of care and investments in consumerism could change thinking about how healthcare should be delivered. Healthcare could shift away from a “build it and they will come” mind-set and toward assumptions in other services industries, where anticipating customers’ needs, digital marketing, and consumer shopping are essential.

Chronic disease management that works. The strategy of establishing standardized clinical pathways has lacked the intensity needed to drive behavioral change. New strategies based on redesigned incentives could use digital approaches to keep patients, providers, and payers more closely engaged with each other. For example, some of the top US payers are now offering members access to cellular-phone-connected glucose monitoring that issues an alert if a patient’s blood glucose is too low.

Automation that changes the cost of care. Capability improvements could make it possible to apply advanced analytics and automation to clinical and operational workflows to increase asset utilization, reduce clinical variability, and streamline labor-intensive processes. Integration of analytics into existing clinical information systems is a key opportunity to be unlocked. The need to better control the cost of care delivery positions the market for faster adoption of effective solutions.

New approaches for post-acute care. The traditional “buy it and fix it” approach that many institutional investors have used for post-acute care has proved that it is not sufficient to simply develop a more efficient version of the same business model. Given the demands for “aging in place” from consumers and lower post-acute costs from payers, effective home health and remote monitoring solutions could disrupt the market. Should this occur, the facility-based post-acute market will need to further restructure.

Carve-out of elective ancillary revenues from hospitals. Investments are expanding from primary care groups to specialist and multi-specialty groups that own ambulatory surgery and other ancillary facilities (e.g., diagnostic imaging, lab, pharmacy, and intermediate care). This shift is likely to create physician organizations that can cater to consumers’ one-stop-shop preferences and take risk by providing lower-cost alternatives, thereby supporting payers’ efforts at medical management. As a result, referral networks for elective care could consolidate and lower-acuity elective services would continue to shift out of hospitals.

Next generation of revenue cycle innovation. A greater focus on the intersection of patients, providers, and payers in healthcare payments, coupled with predictive analytics and consumer engagement, could breathe new life into the marketplace. This change could make possible new tools that would enable payers and providers to determine and adjudicate complex claims more effectively as well as give patients a simpler payments process.

Even if only half the investments from institutional investors are successful, the resulting industry shifts could reduce variability in care delivery, optimize appropriate sites of care, and lower the overall cost of care. Over the past decade, the annual increase in national health expenditures has averaged just over 4%.14 We believe that the trend curve could be bent—it is even possible that the cost curve could become negative (temporarily, at least) if enough waste if driven out of the system.

How providers could respond

We believe that future investments will need to be more directive and have a clearer ROIC, given the amount of capital being put into healthcare. Therefore, health systems will need to think differently about their role: Will they become leaders or followers in helping shape the industry’s future? There are a few directions a health system could take, depending on its business strategy and access to capital.

Become an active investor. Some health systems may want to take the cue from institutional investors and continue to diversify their investments and sources of revenues in healthcare services. These health systems could invest to build capabilities de novo, given their expertise in local markets, or compete with institutional investors on deals. Since 2012, health systems have engaged in nearly 1,000 transactions, and those that have successfully diversified their portfolios to include high-return ancillary assets have achieved stronger performance than their peers (nearly 10% ROIC versus less than 5% for a simple hospital network).15 However, becoming an active investor requires access to capital and a willingness to divert strategic capital to new businesses with longer timelines for returns.

Partner with institutional investors. Institutional investors will continue to buy assets across the healthcare continuum, which creates a range of partnership opportunities for health systems, including joint venture structures for acquisitions, and preferred contractual relationships with PE-backed portfolio companies. Such partnerships could be mutually beneficial to both parties. Health systems would benefit from improved offerings tailored to their markets or unmet needs, as well as having access to part of the upside gains. Institutional investors would be able to scale their investments more quickly, resulting in higher value generation. However, these arrangements may be complex to manage, and there could be differences between an institutional investor’s and the health system’s expectations for returns. Additionally, for select not-for-profit health systems, there could be tension between investing in a community mission (e.g., serving Medicaid patients) and investing in revenue diversification.

Wait to acquire scaled business models. Over several years, institutional investors could potentially aggregate assets and create platforms of scale. These platforms might be attractive acquisition targets for health systems that want to accelerate their business model evolution with less risk. Health systems that want to use this approach would have to be able to afford a premium, given that PE buying sprees create scale and often result in a shortage of supply, which expands multiples. The increase in costs likely helps explain why health system acquisition activity has cooled off recently (there were only about 100 transactions in 2017, compared with about 230 two years earlier). Another drawback is that this approach requires health systems to wait and may create a window for new entrants, (e.g., payers) to acquire healthcare services assets.

Health systems will also need to put defensive strategies in place. The new business models likely to emerge from institutional investments will probably continue the longer-term trend of reducing care delivery in hospitals. This will disproportionately affect health systems with high cost structures, insufficient quality outcomes, and/or an inadequate consumer experience. Furthermore, the scale-up of non-hospital services will decrease health systems’ negotiating leverage (e.g., with an existing anesthesiology group or revenue cycle management vendor)—a problem that will be particularly acute for smaller health systems. These pressures will increase the imperative for health systems to continue to evolve their business models to focus on delivering high-quality healthcare, to make sure their operating models have a dual focus on cost management and quality and to build capabilities to integrate with new healthcare services partners into an ecosystem to create value.

The silent shapers of healthcare are here to stay. Their investments are likely to accelerate and have even deeper impact. We believe it is crucial that health systems not attempt to maintain the status quo or be passive observers of market restructuring. The longer a health system waits to become part of the industry’s changes, the costlier the impact will be—its current business model could further erode, and entering new markets will likely become more expensive.

New, proactive tactics are needed regardless of the degree of active investment. Such an approach will allow health systems not only to preserve economics and share the market with institutional investors, but also to shape how and where care is delivered to patients.

About the author(s)

Neha Patel is a partner in McKinsey’s New Jersey office. Lisa Foo is an associate partner in the San Francisco office. Saum Sutaria, MD is a senior partner in the Silicon Valley office.

The authors would like to thank Prashanth Reddy, Nick Petersdorf, Lara Sanfilippo, Manuel Valverde, and Ellen Rosen for their support and assistance in preparing this article.

Article link: https://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/the-silent-shapers-of-healthcare-services